ABA numbers play a crucial role in the banking system, ensuring seamless and accurate transactions between financial institutions. If you've ever wondered what an ABA number is and how it works, this guide will provide you with all the information you need. From its definition to its applications, we will delve into the intricacies of ABA routing numbers and their significance in the financial world.

Banking processes can sometimes seem complicated, especially when it comes to understanding the various codes and numbers associated with transactions. However, having a clear understanding of ABA numbers can help simplify your banking experience. In this article, we will explore the history, purpose, and functionality of ABA numbers to give you a comprehensive understanding of their importance.

As we navigate through the complexities of modern banking, knowing the role of ABA numbers can enhance your ability to manage your finances effectively. Whether you're making a wire transfer, setting up direct deposits, or paying bills online, ABA numbers are essential for ensuring that your money reaches the right destination. Let's dive deeper into the world of ABA numbers and uncover their significance.

Read also:Mugshots Bullitt County Ky

Table of Contents

- What is an ABA Number?

- History of ABA Numbers

- Structure of an ABA Number

- Common Uses of ABA Numbers

- Difference Between ABA and ACH Numbers

- Why Are ABA Numbers Important?

- How to Find Your ABA Number

- Security Measures for ABA Numbers

- Common Errors When Using ABA Numbers

- Frequently Asked Questions About ABA Numbers

- Conclusion

What is an ABA Number?

An ABA number, also known as a routing transit number (RTN), is a unique nine-digit code assigned to financial institutions in the United States. This number identifies the specific bank or credit union involved in a financial transaction. It plays a critical role in directing funds to the correct institution, ensuring that payments, deposits, and transfers are processed accurately.

The ABA number was originally developed by the American Bankers Association (ABA) in 1910 to standardize the banking system. Today, it remains an essential component of the U.S. financial infrastructure, facilitating various types of transactions.

How Does an ABA Number Work?

When you initiate a transaction, such as a direct deposit or wire transfer, the ABA number is used to route the funds to the appropriate bank. Each bank or credit union has its own unique ABA number, which is embedded in the routing process to ensure precision and security.

- Identifies the financial institution involved in the transaction.

- Facilitates the transfer of funds between banks.

- Ensures accurate processing of payments and deposits.

History of ABA Numbers

The concept of ABA numbers dates back to 1910 when the American Bankers Association introduced them to streamline the check clearing process. At the time, the banking system lacked a standardized method for identifying financial institutions, leading to inefficiencies and errors in transactions. The creation of ABA numbers addressed this issue by providing a unique identifier for each bank or credit union.

Over the years, the use of ABA numbers has expanded beyond check processing to include electronic transactions such as direct deposits, wire transfers, and automated clearing house (ACH) payments. Today, ABA numbers are an integral part of the U.S. banking system, ensuring the smooth flow of funds between financial institutions.

Structure of an ABA Number

An ABA number consists of nine digits, each serving a specific purpose. Here's a breakdown of the structure:

Read also:Winery At Perennial Vineyards

- Digits 1-4: Federal Reserve Routing Symbol – Identifies the Federal Reserve Bank responsible for processing the transaction.

- Digits 5-8: Institution Identifier – Identifies the specific bank or credit union.

- Digit 9: Check Digit – Used to verify the accuracy of the ABA number.

This structured format ensures that ABA numbers are unique and can be easily validated during transactions.

Common Uses of ABA Numbers

ABA numbers are used in various financial transactions, including:

- Direct Deposits: Employers use ABA numbers to deposit employees' salaries directly into their bank accounts.

- Wire Transfers: ABA numbers are essential for transferring funds between banks, especially for international transactions.

- Bill Payments: Many online bill payment services require an ABA number to ensure that payments are directed to the correct financial institution.

- ACH Transfers: Automated Clearing House (ACH) transactions rely on ABA numbers to process payments and transfers efficiently.

Understanding the various uses of ABA numbers can help you navigate the banking system more effectively.

Difference Between ABA and ACH Numbers

While ABA numbers and ACH numbers are often used interchangeably, they serve slightly different purposes:

- ABA Numbers: Primarily used for wire transfers and check processing.

- ACH Numbers: Specifically designed for electronic transactions, such as direct deposits and bill payments.

In some cases, the ABA number and ACH number for a particular bank may be the same. However, it's important to verify the correct number to ensure accurate transaction processing.

Why Do Banks Have Different ABA and ACH Numbers?

Banks may use different ABA and ACH numbers to streamline their internal processes and improve transaction efficiency. For example, a bank might designate one ABA number for wire transfers and another for ACH transactions to better manage the flow of funds.

Why Are ABA Numbers Important?

ABA numbers are crucial for maintaining the integrity of the U.S. banking system. They ensure that financial transactions are processed accurately and securely, reducing the risk of errors and fraud. By providing a unique identifier for each financial institution, ABA numbers help facilitate the smooth transfer of funds between banks.

In addition to their practical applications, ABA numbers contribute to the overall trust and reliability of the banking system. They enable individuals and businesses to conduct financial transactions with confidence, knowing that their money will reach the intended destination.

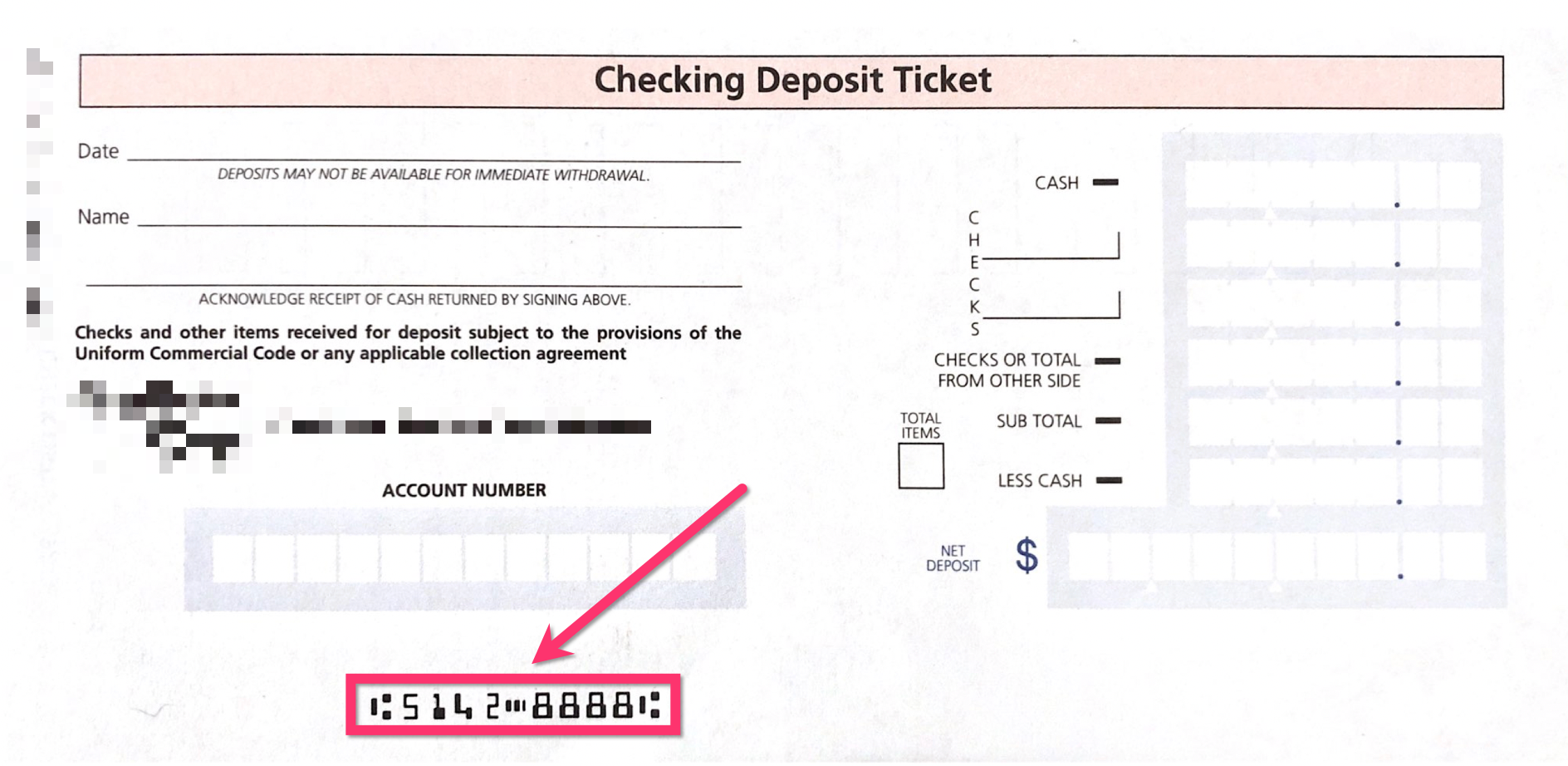

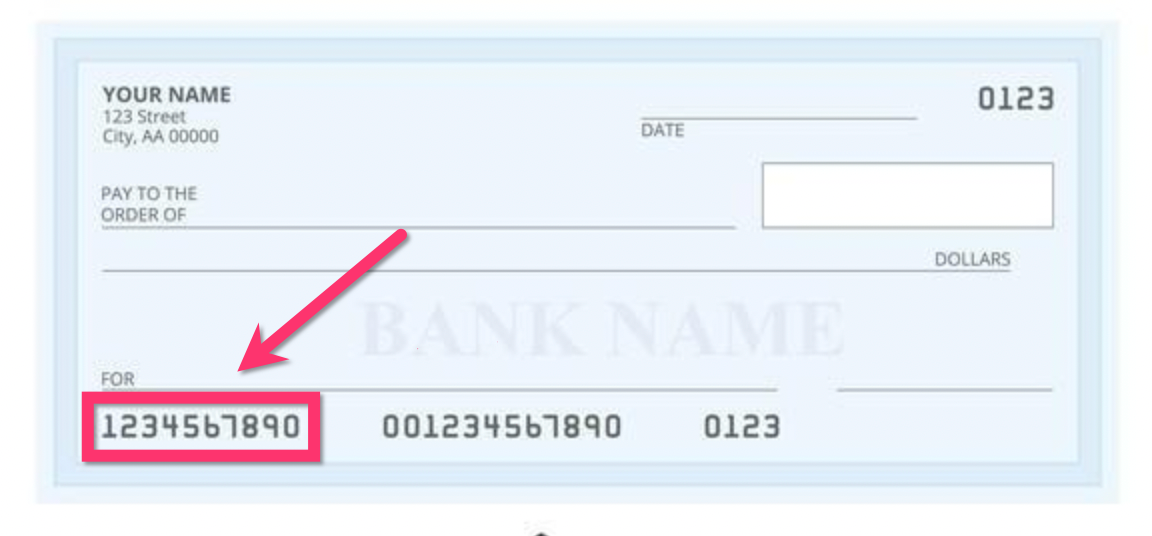

How to Find Your ABA Number

Locating your ABA number is a straightforward process. Here are some common methods:

- Bank Statement: Your ABA number is typically listed on your bank statement, either online or in print.

- Checkbook: The ABA number is printed on the bottom left corner of your checks, usually as the first set of numbers.

- Bank Website: Many banks provide ABA numbers on their websites, often in the account information section.

- Customer Service: If you're unable to locate your ABA number, you can contact your bank's customer service department for assistance.

It's important to verify the correct ABA number for your specific account, as some banks may have different numbers for different types of transactions.

Security Measures for ABA Numbers

Protecting your ABA number is essential to prevent unauthorized access and potential fraud. Here are some security tips:

- Keep Your Information Private: Avoid sharing your ABA number with unauthorized individuals or unsecured websites.

- Monitor Your Accounts: Regularly review your bank statements for any suspicious activity.

- Use Secure Connections: When accessing your bank account online, ensure that you're using a secure and encrypted connection.

By taking these precautions, you can help safeguard your financial information and protect yourself from potential fraud.

What to Do if Your ABA Number is Compromised

If you suspect that your ABA number has been compromised, contact your bank immediately to report the issue. Your bank can provide guidance on the necessary steps to secure your account and prevent further unauthorized access.

Common Errors When Using ABA Numbers

When using ABA numbers for transactions, it's important to avoid common mistakes that could lead to processing errors or delays. Some of these errors include:

- Incorrect Number Entry: Double-check the ABA number to ensure accuracy before initiating a transaction.

- Using the Wrong Number: Verify whether you need the ABA number or ACH number for the specific transaction.

- Missing Digits: Ensure that all nine digits of the ABA number are included in the transaction details.

By paying attention to these details, you can help ensure that your transactions are processed smoothly and efficiently.

Frequently Asked Questions About ABA Numbers

Q: Can I Use the Same ABA Number for All Transactions?

It depends on your bank and the type of transaction. Some banks use the same ABA number for all transactions, while others may have different numbers for wire transfers and ACH transactions. Always verify the correct number with your bank to avoid processing errors.

Q: Are ABA Numbers Unique to Each Bank?

Yes, each bank or credit union in the United States has its own unique ABA number. This ensures that transactions are routed to the correct financial institution.

Q: Can I Find My ABA Number Online?

Many banks provide ABA numbers on their websites, but it's important to ensure that you're accessing this information through a secure and legitimate source. If you're unsure, contact your bank's customer service department for confirmation.

Conclusion

ABA numbers are an essential component of the U.S. banking system, ensuring the accurate and secure processing of financial transactions. By understanding their structure, uses, and importance, you can better manage your finances and avoid common errors that could lead to delays or inaccuracies.

We encourage you to share this article with others who may benefit from learning about ABA numbers. If you have any questions or comments, feel free to leave them below. Additionally, explore our other resources on personal finance and banking to further enhance your knowledge and skills.

Sources: